Popular Posts

If you’re reading these words, I’d wager it’s because the headline piqued your interest. From that, it seems clear that you already know what an IRA is and think you might need one.

Mostly probably, though, you don’t have one. But you should, and you probably should have two. Let me explain why.

If you have a job with a salary, you are very likely to have access to a 401(k), 403(b) or a 457 plan. The differences in these plans are minor; they all do the same thing roughly the same way, that is, they help you save for retirement.

The reason you want a workplace plan is because it helps you lower your taxes today and helps you to save more. Your contributions grow tax-free until retirement and, in many jobs, your employer will match your contributions in part. Both of these facts mean free money for you.

So why bother with an individual retirement account (IRA)? Well, if you know for fact that you will work at the same job for 40 years, you might not need one. However, if you expect to change jobs in the future, have an unemployed spouse or any need for tax-free income in retirement, well, that’s what an IRA does.

You can open one at any bank or brokerage house you like. Your ability to put money into an IRA has some limits. If you already maximize your workplace plan, it’s hard to put away more in an IRA and still get a deduction for it. Contributing to a non-working spouse’s plan is the exception.

If you’re not going to get a current year deduction for a traditional IRA, consider opening a Roth IRA instead. That money will grow tax-free and can be withdrawn later tax-free, too. Plus, the rules around required distributions and withdrawals are far more forgiving.

This can get complicated quick, so it’s worthwhile to consult a tax preparer and to become a student of the IRA game. Nevertheless, one last point is important to remember: Remember to open an IRA once you leave your current job.

The reason why is rollovers. You have the right to roll money out of your 401(k) plan and into an IRA once you leave a job. Over the course of a career this might happen several times.

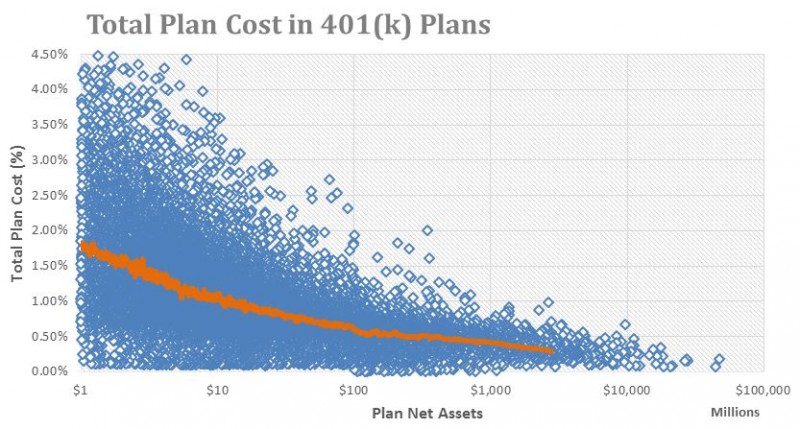

Now, you could leave the money in your old company plan, that’s true. However, the fees in corporate 401(k) plans are often extraordinarily high. Brightscope, a firm that analyzes workplace plans, found that only when a plan is managing well over $100 million do fees become reasonably low.

Since they are smaller, most small company plans charge more. Nevertheless, you can remove money from old 401(k) plans and manage it yourself in an IRA using ETFs at a fraction of the cost.

Bottom line: Use your 401(k) to the hilt while you’re there, or at least enough to capture the tax breaks and matching money. Maximize your tax-free income for later with a Roth. And never leave money stranded in a pricey workplace plan once you move on.

Sign Up for Our

Free Email Newsletter