Popular Posts

It has been hard over the past few months to avoid news about the Federal Reserve and interest rates going up.

Rates have not gone up by much at a time, a quarter point every few months. The U.S. monetary authority seems to be sticking to its long forecast plan of steady but highly predictable changes.

So why is this news, and what should investors do about it — if anything?

First, it’s news because the U.S. benchmark interest rate was virtually zero for a very long time.

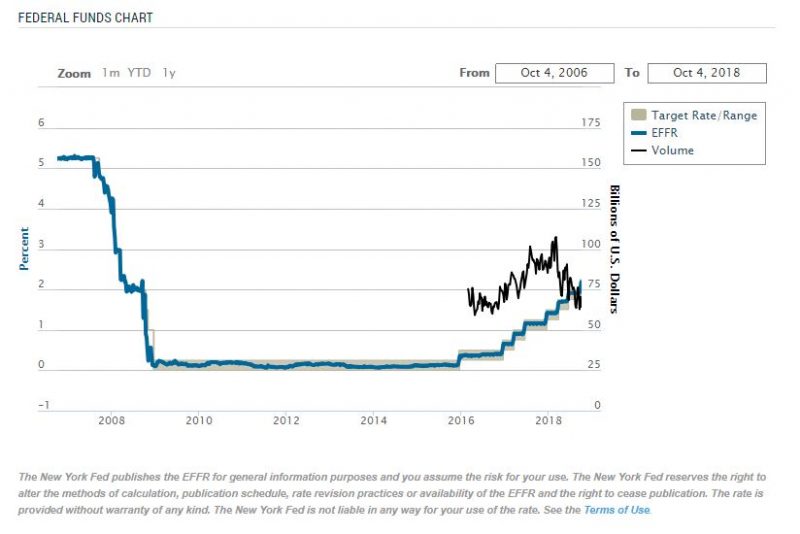

The federal funds rate, as it’s called, was at 5.25 percent before the 2008 crisis. It fell very quickly to well under 0.25 percent and stayed there until December 2015.

The target rate of between zero and 0.25 percent was the Fed’s way of supporting the U.S. economy during Great Recession. By making money virtually free, the Fed effectively put its weight behind the banks.

Low borrowing rates on mortgages and car loans goosed up housing, autos, business growth, exports — everything.

Historians will have to sort out whether the plan was a success or a failure. The issue now is that, after many years of hovering near zero, we’re back on path upward, recently targeting between 2 percent and 2.25 percent.

The Fed has promised more to come, albeit gradually. It continues to telegraph the changes so as not to surprise investors either way.

So what does it mean for people trying to save and invest for the long term?

In the immediate sense, a rising interest rate means that interest-paying investments such as checking accounts, certificates of deposit, bonds and bond funds will pay more interest.

That’s a big change. Investors in need of income, such as retirees, had been relying on alternative forms of income investing, including real estate funds and dividend-paying stocks.

Yet many of those investors would prefer bonds. The risk is lower, depending on what type of bond you own, and the payouts are more reliable.

That doesn’t mean that bonds are “safe” the way, say, a certificate of deposit is considered safe. Bonds can lose value and are not insured by the FDIC.

Nevertheless, over time bonds are safer than stock investments and many government-issued bonds are far safer relative to stocks.

Over time, the income portion of many tens of thousands of investment portfolios will fill back up with bonds. To fund those investments, some people are likely to sell stocks to raise cash.

Does that mean stocks must fall soon? Not necessarily. A rising interest rate is symptomatic of rising inflation, and rising inflating is symptomatic of a fast-growing economy.

Faster growth, of course, bodes well for stock investments. It certainly is better news than slowing growth or a declining economy.

All this means that investors should carefully consider the balance of bonds to stocks in their investment planning. It’s important to ensure that your portfolio is not prone to sharp decline in value — if such a decline would prompt a rash decision on your part.

If not, a decline in stock prices might be just the thing some investors need. A continually rising stock market eventually makes it difficult for investors to continue to buy.

So long as at least some investors are trying to buy low in order to sell high years later, they will need lower prices. It’s really a matter of being certain that the mix of stocks and bonds in your portfolio is a match to your own risk tolerance.

Can you handle watching the stock market decline? Do you consider that good news, or bad? An opportunity or a problem?

Answering these questions honestly, possibly with the help of an advisor, can go a long way toward making sure stay on track toward your investment goals over the long run.

MarketRiders, Inc. is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Sign Up for Our

Free Email Newsletter